Wealthsimple: Financial Optimizer

Quick, personalized and actionable financial advice

Overview

A digital solution designed to address the following problems: many users of the Wealthsimple product do not understand the value of financial advice and our Portfolio Management team is not large enough to communicate that value through 1:1 conversations to all our clients at scale.

I spearheaded this project while working as a Portfolio Manager at Wealthsimple

The final solution was a short questionnaire offered to clients to understand their financial situation and provide them with personalized financial advice and actionable insights generated based on their inputs.

I supplemented this case study with a prototype of the Financial Optimizer that I created independently, with the use of the Wealthsimple design system.

Context

Currently, all clients are not aware that they can receive financial advice from a member of the Portfolio Management team. Clients with deposits over $100,000 qualify for the Wealthsimple Black program where they can receive in-depth financial planning services and develop an ongoing 1:1 relationship with a dedicated Portfolio Manager.

A common observation when engaging with clients is that they don’t understand the value of financial advice. We wanted to find a low-barrier solution to provide advice and demonstrate its value, ultimately motivating clients to deposit more to their accounts. However, even if all clients were to understand the value of advice, our team is too small to provide that advice one-on-one to millions of clients. Our low-barrier solution needs to offer advice at scale.

Research

According to Vanguard, the value of advice equates to an additional 3% annual return.

“ We believe implementing the Vanguard Advisor’s Alpha framework can add about 3% in net returns for your clients and also allow you to differentiate your skills and practice.”

How do we bring this value to all our clients, not just the the ones with 1:1 relationships with advisors?

Hypothesis

We believe that we can demonstrate the value of advice by providing clients with a low-barrier solution to receive financial advice.

We will know this is true if clients contribute additional amounts to their accounts to qualify for higher tiers like Wealthsimple Black in order to receive 1:1 guidance from a Portfolio Manager.

Ideation

I began to brainstorm solutions with the following question in mind:

How might Portfolio Managers reach our 1M+ clients at scale, in order to provide each one with financial advice?

In order to prioritize solutions/ the various mediums through which we could provide advice, I set three constraints/ requirements for the outcome we would need to achieve.

The advice should be personalized to the individual or to the group.

Clients should have actionable takeaways for next steps to achieving their goal.

The solution should be easily accessible for all clients.

Solution

Based on our constraints, we felt that the most appropriate solution would be an in-product survey that would collect information on client goals, savings, income, expenses and more. With this information, we can then provide them with personalized financial advice and some action items that can help to maximize a client’s chances of achieving their financial goals.

The challenge was that we would have to prove this hypothesis on our own, before we could reasonably request resources from product and engineering teams, who were working towards other business goals. If we could validate the hypothesis by working around these constraints, we could build a proposal to receive additional resources.

I started by using tools such as Typeform and Excel to collect information, and then built a model that would incorporate our logic to present recommendations based on client inputs to the survey.

Our solution went through three main iterations. The employee test, our first user test and finally an iteration based on user feedback.

The employee test allowed us to assess interest in our solution, and collect initial feedback. We had 25 employees sign up and provide feedback which helped us address gaps in our logic and make adjustments to simplify the language in our recommendations.

With a successful employee test, we sent out the survey to 1000 clients and received a 15% response rate. The response rate was higher than the general click through rate for all emails, suggesting high levels of interest from clients.

Impact

When assessing the results one month after sending the recommendations, we found that survey respondents deposited $3800 to their accounts on average, compared to $1200 deposited by unresponsive recipients and $1100 by the control group.

90.50% of survey participants deposited money after receiving the survey compared to 72.71% of unresponsive clients and 75.10% of the control group. While the sample size was small at this point, we think a tool like this could help with conversion from registrant to client - which would need to be tested separately.

User feedback

Common feedback heard from respondents was that the recommendations took too long to receive. Although the logic was built for recommendations to be automatically generated based on results, each client had to be manually emailed their recommendations as we didn’t have the technology built to send out automated responses.

The recommendations also felt generic and not personalized:

“The advice was just generic copy and paste advice. I understand that there's a lot of clients to provide feedback to, but if it's not possible to provide something that is specific to the situation or to the goals I listed, then it shouldn't have been offered in the first place.”

Some clients expressed a need to complete such a process through the product itself

“I also think the recommendations tool would be more useful if there was a way to take it via my profile online so that my responses are visible for later and so are the recommendations (vs. having to keep track of the email you'd sent). If I could get the messaging from you directly through the WealthSimple site, that would be even better (as then I'm still getting recommendations directly from you but it's all kept to the website in one central place).”

We started by tackling the feedback that the advice felt generic by updating the format through which the recommendations were sent. We sent the survey to another round of clients, this time delivering the recommendations in a PDF format instead of an email.

While this process felt more well designed and the projections made the recommendations feel more personalized, the delivered document felt complex and it still took time for clients to receive their recommendations from our team after submitting answers due to the time required to fill in and create the document. Ultimately, clients still preferred an in-product experience.

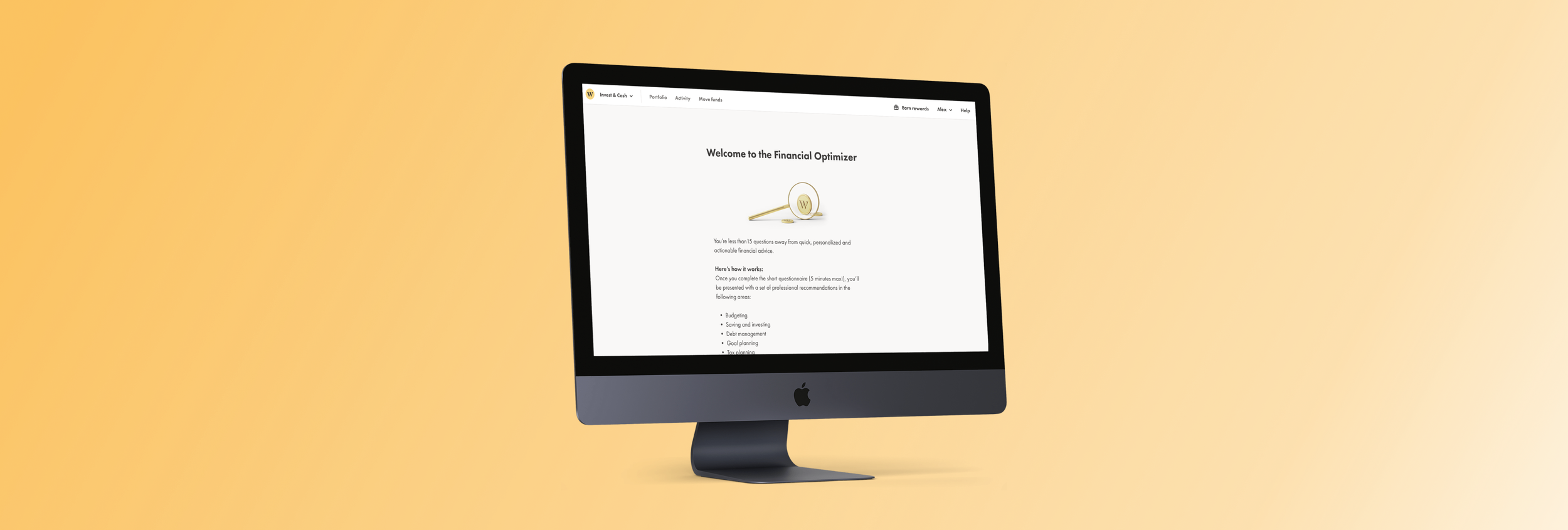

Prototype

I believe that if clients were to receive “standardized” responses immediately after submitting answers, they would find more value in the recommendations provided as the “cookie-cutter” responses would meet their expectations of an automated system. With the emailed recommendations as well as the tailored PDF, clients were still working within the mental model of interacting with a human advisor, while we were interested in testing an automated experience.

Ultimately, we were not able to test out an in-app experience of the Financial Optimizer, due to business constraints and a lack of resources. After developing my skill-set in the UX and UI Design discipline, I independently developed a hypothetical prototype of what this project could look like in product.

Key Learnings

Using the Wealthsimple design system; working within the constraints of an established design system was a different experience to building an app from scratch as I had done previously for my capstone project, Advisr. A design system made it simpler and faster to build out a working prototype, which would allow me to validate my assumptions more efficiently.

However, it was difficult to make UX improvements if there were elements missing from the design system. For example, in the Wealthsimple design system, there were no progress indicators for forms. I was unable to display how many steps were left for the user to complete.

Additionally, feedback at each iteration was crucial for testing out our hypothesis. While the early data around client deposits was promising, the feedback suggested there were significant improvements to be made to make this feature viable.

Lastly, I learnt that in order to test out a solution, it’s important for the prototype to be as close to the real experience as possible. With our stand-in solution of emailing clients, we were working within the mental model of an advisor/ client relationship as opposed to in-product recommendations - which remained the focus of most clients’ feedback, preventing us from validating our initial hypothesis.